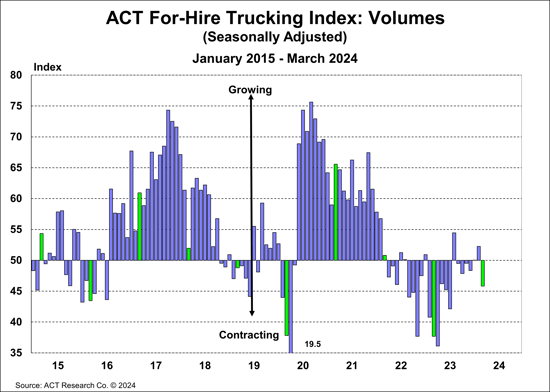

VOLUME INDEX:

The Volume Index decreased 6.5 points in March to 45.8, seasonally adjusted (SA), from 52.3 in February. The low volume reading in March likely reflects that the Chinese New Year started three weeks later this year in mid-February, and some carriers are losing contractual volume this bidding season as they reject unsustainable offers from shippers.

While volumes remain broadly soft, the continuing strength of the US economy, alongside slowing capacity additions, gives us reason to think volumes will gradually improve in 2024. Inflation risk remains, but y/y declines in goods prices in recent months, while small, should help demand, as reflected by strong March US retail sales. Additionally, after a significant destock that began in mid-2022, loaded NA imports were up 26% y/y in February, though the later-than-usual Chinese New Year will likely result in lower March volumes.

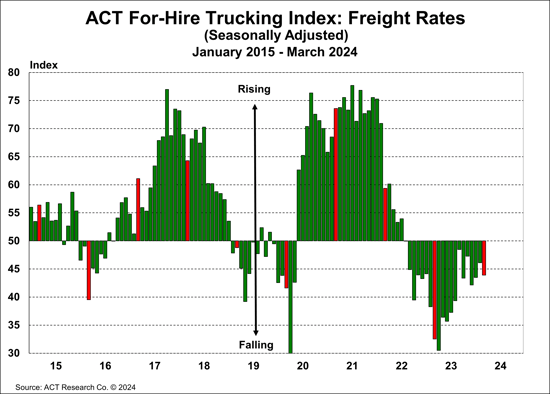

PRICING INDEX:

PRICING INDEX:

The Pricing Index fell 2.2 points in March to 43.9 (SA), as the freight market retrenched following the rise in rates in February due to the cold weather snap that affected much of the country in January, but spot rates remain 5¢ above the Q4 average. The market still favors shippers, as capacity additions by private fleets last year weighed on for-hire fleets, but most recent Class 8 tractor order and sales data show a decline in equipment additions, a requisite for rates to improve meaningfully. Though fleet capacity growth has delayed the recovery in rates, the improving supply/demand balance suggests the worst is in the rearview, and the cyclical recovery should continue.

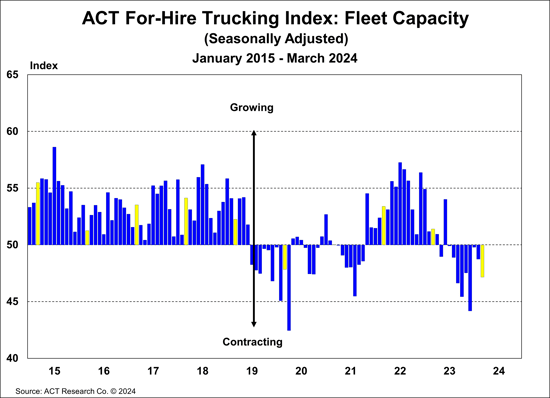

CAPACITY INDEX:

The Capacity Index decreased by 1.5 points m/m to 47.2 in March. The decrease continues to reflect challenging for-hire conditions, with low rates and higher costs making profitability hard to come by. As such, for-hire capacity has contracted for the past nine months, and with many large fleets lowering capex budgets in 2024 and delaying additions, capacity declines are likely to continue.

Class 8 sales trends suggest the ongoing capacity additions at private fleets, a key reason the downcycle has drawn out so long, are slowing too, reducing overall capacity additions and downward rate pressure.

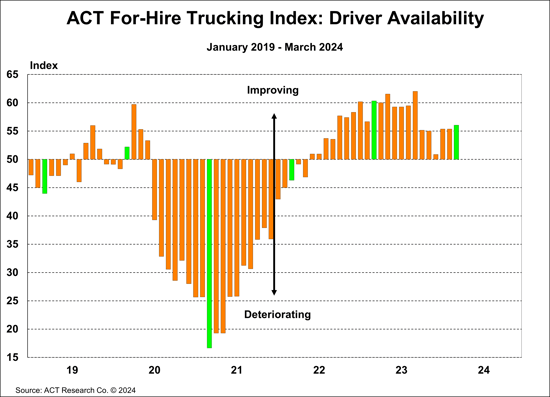

DRIVERS:

DRIVERS:

The Driver Availability Index ticked up to 56.0 in March, from 55.4 in February. The resilience may be due in part to the softness in volumes (note we have not yet seasonally adjusted this index), but driver availability remains persistently elevated and far from a shortage.

Downward pressure should resume as driver availability has a long cyclical lag, and higher-paying construction and manufacturing jobs should provide more competition for drivers this year. Competition from higher-paying private fleets is also likely to press driver availability lower. Baby boomer retirements should continue, but our survey also found drivers delaying retirement because of the recent surge in inflation. One even noted some of their best “runners” are past retirement age.

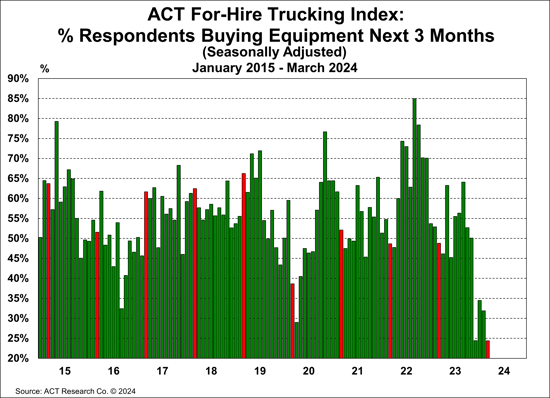

FLEET PURCHASE INTENTIONS:

Fleet purchase intentions decreased 7.5 percentage points m/m to the lowest March reading on record, with only 24.0% of respondents saying they plan to buy equipment in the next three months, compared to the 56.0% historical average. Simply put: truckers don’t buy trucks when they aren’t making money. The low profitability environment has resulted in many large fleets cutting capex budgets by as much as 30-40%, with some even delaying equipment purchases. When rates improve, purchasing sentiment should follow.

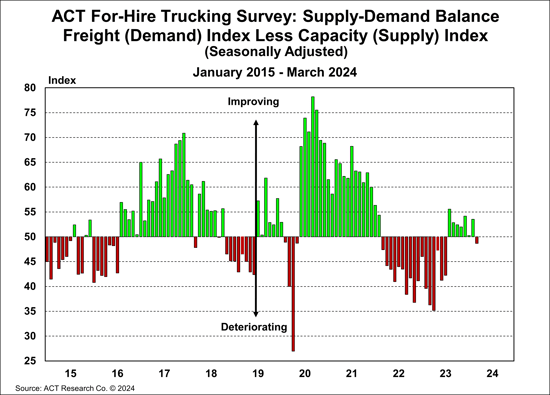

SUPPLY-DEMAND BALANCE:

SUPPLY-DEMAND BALANCE:

The Supply-Demand Balance turned down in March to 48.7 (SA), from 53.5 in February, as volumes decreased more than capacity. This breaks a seven-month streak with the Supply-Demand Balance in positive territory, mainly due to capacity contraction. Recent green shoots suggest the gradually improving volume trends will improve the market balance in 2024. Overall, the Supply-Demand Balance suggests a market close to the elusive and impermanent equilibrium.

Despite the March pullback, which was partly temporary, improving cyclical dynamics are continuing. Rising goods demand and the end of inventory destocking are leading to strong improvements in imports and intermodal volumes. The problem remains that the economic strength is being handled by private fleets who continue to add capacity in 2024, more than two years after the market balance turned. But this dynamic is shifting, and while it will take time, cost economics should disincentivize further additions and press freight to the for-hire market.

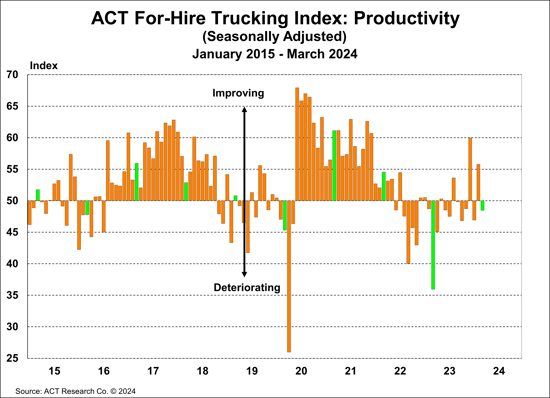

PRODUCTIVITY INDEX:

(miles/tractor)

Fleet productivity fell 7.3 points m/m, to 48.5 (SA) in March, consistent with the lower reading for the Volume Index. Productivity remains challenged by lingering looseness in the for-hire market but should gradually improve with volume increases and continued capacity decreases.